Bank Negara Malaysia (BNM) has announced a major policy intervention to end payment fragmentation by ordering a complete phaseout of all proprietary and closed-loop QR payment networks within the next two years.

According to the freshly enacted Interoperable Fund Transfer Framework (IFTF) policy document, all existing exclusive QR schemes must be entirely discontinued by June 30, 2028. To prevent further market fragmentation during this transition, the central bank has banned all affected financial institutions and e-wallet operators from onboarding any new merchants onto their proprietary networks with immediate effect.

Standardising the Cashless Ecosystem

The structural shift ensures that consumers will no longer need to navigate a maze of separate, incompatible QR codes displayed at retail counters. Moving forward, any participating mobile banking or e-wallet application will be capable of clearing payments seamlessly across a single, unified network.

Under the new regulatory baseline, the division of labor across the network is explicitly mandated,

- Banking Obligations – Commercial banks offering retail QR solutions must participate in the national shared payment infrastructure, permitting their retail client base to pay any merchant, regardless of the merchant’s acquiring institution.

- Acquirer Obligations – Merchant-acquirers must similarly configure their infrastructure to accept financial routing from any participating domestic or non-bank digital money account.

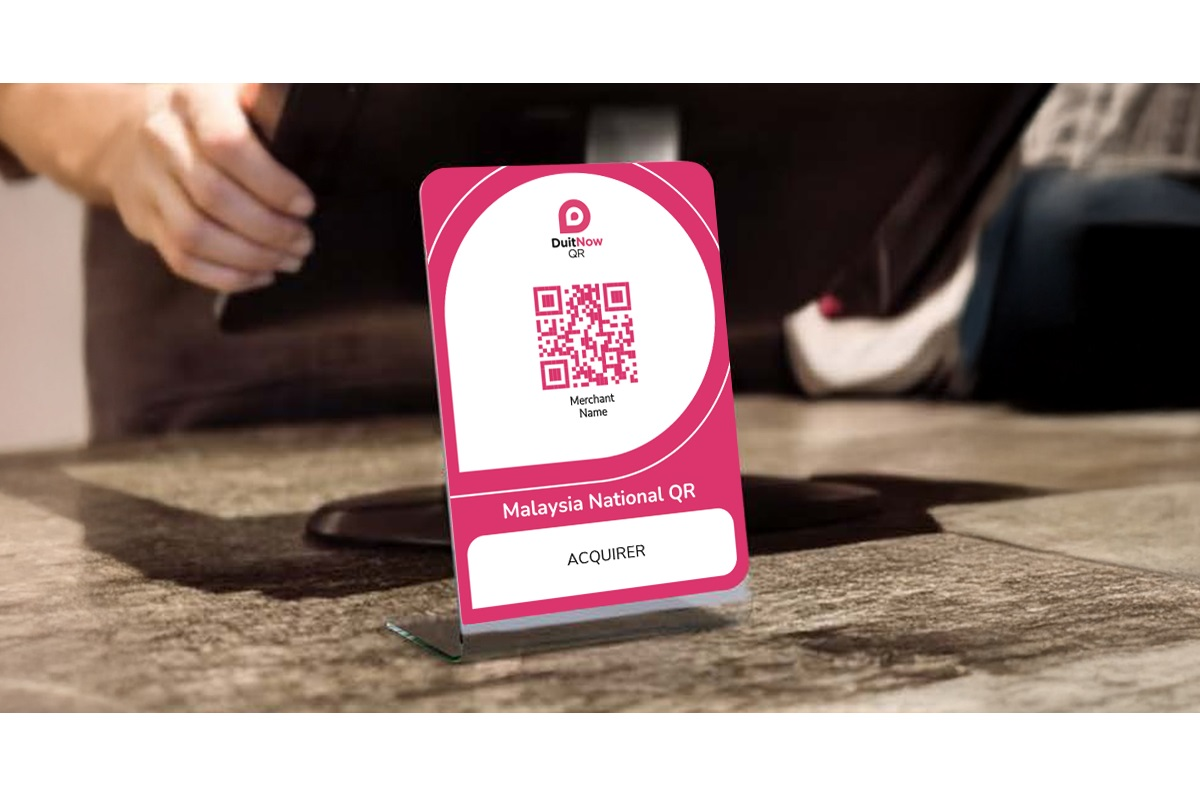

The core of this unified ecosystem rests upon the Real-time Retail Payments Platform, which powers ubiquitous consumer services like DuitNow Transfer and DuitNow QR. This infrastructure is managed by PayNet, an entity 35.5%-owned by BNM, with the remaining equity distributed across 11 major Malaysian banking institutions.

Balancing High Adoption with Corporate Concerns

The central bank’s regulatory push arrives amid an explosive surge in digital payment adoption across the country. Driven primarily by mobile banking preferences, electronic transactions have reached a historical high, with the average Malaysian now executing at least 1.5 digital payment transactions every day.

Public feedback gathered during prior consultation phases revealed that the vast majority of industry stakeholders supported the termination of proprietary QR schemes, acknowledging that it dramatically improves consumer convenience.

However, a few providers raised corporate anxieties regarding systemic migration costs and potential limitations on their proprietary ability to offer exclusive, closed-loop loyalty and marketing campaigns. Addressing these operational concerns, BNM clarified that the two-year window offers ample time for model adjustments, while PayNet has committed to building structural flexibility within the shared national network so participants can continue designing customized marketing incentives and value-added services.